Changing your health insurance is stressful enough without worrying about whether your daily medications will suddenly cost a fortune. You might think that because you take generic drugs-the cheaper alternatives to brand-name prescriptions-you’re safe from huge price hikes. But that assumption can be dangerous. The reality is that not all generics are treated equally by insurance companies.

When you switch plans, the structure of the new plan’s formulary (the list of covered drugs) determines what you pay. A generic drug that cost $5 under your old plan might jump to $40 or even require you to meet a high deductible first under the new one. Understanding how these tiers work isn’t just about saving money; it’s about ensuring you can actually afford to stay healthy. This guide breaks down exactly how to evaluate generic drug coverage so you don’t get blindsided by surprise bills.

Understanding Formulary Tiers and Generic Drugs

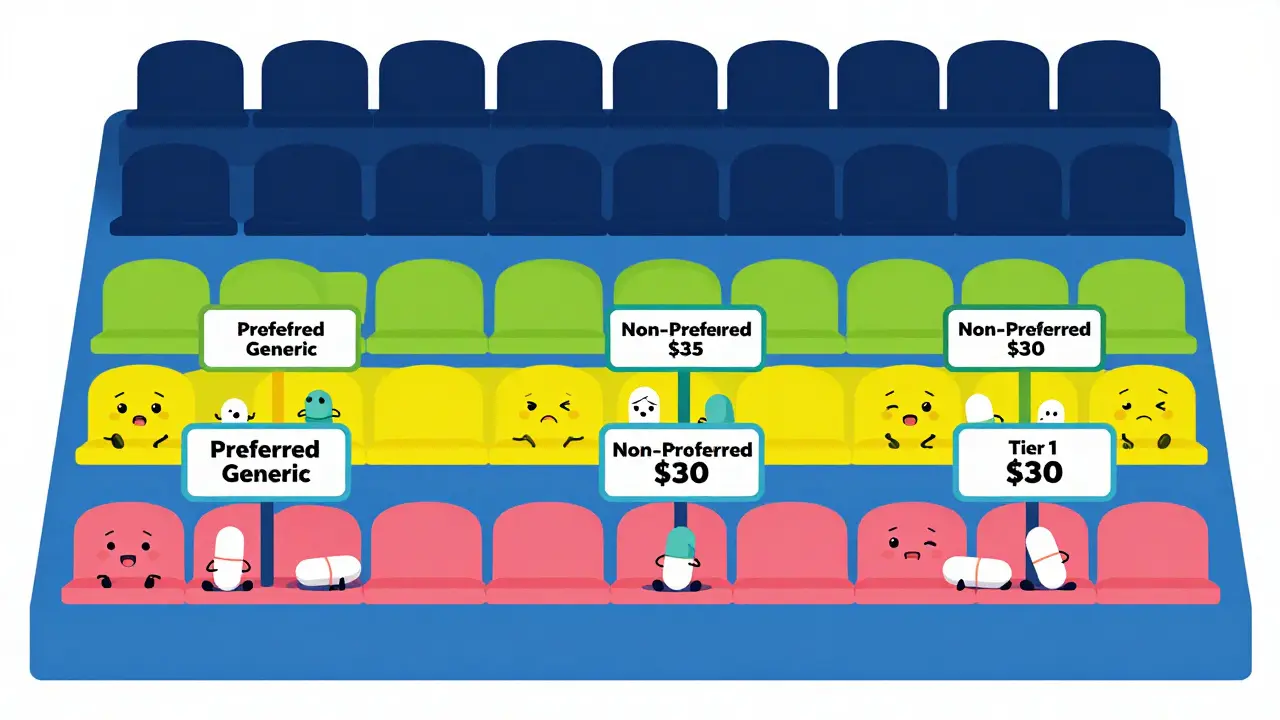

To navigate health plans, you first need to understand the language insurers use. Most plans organize their covered drugs into formularies with tiered structures that dictate your out-of-pocket costs. Think of these tiers like seating sections in a stadium. Tier 1 is the cheapest seat-usually reserved for preferred generic drugs. Tier 2 might include non-preferred generics or lower-cost brand names. Higher tiers (3, 4, and 5) are for expensive specialty medications.

The key insight here is that "generic" doesn’t always mean "Tier 1." Some plans split generics into two categories: preferred generics (Tier 1) and non-preferred generics (often Tier 2). Why would a generic be non-preferred? Usually, it comes down to which manufacturer makes it. If your doctor prescribes a specific generic made by Company A, but your insurance prefers the same drug made by Company B, you might face higher costs unless your doctor switches the manufacturer. This distinction is critical when comparing plans.

| Plan Type | Typical Generic Copay | Deductible Impact | Best For |

|---|---|---|---|

| Silver SPD (Marketplace) | $10-$20 fixed | Waived for Tier 1 generics | People on regular maintenance meds |

| High-Deductible Health Plan (HDHP) | Varies (often % coinsurance) | Must meet full deductible first* | Healthy individuals rarely needing meds |

| Medicare Advantage (MA-PD) | $0-$10 copay | Usually low or no deductible for generics | Seniors wanting predictable costs |

| Employer-Sponsored PPO | $5-$15 copay | Depends on plan design | Employees with comprehensive benefits |

*Note: Some Silver Standardized Plan Designs (SPDs) waive the deductible specifically for Tier 1 generics, allowing you to pay a flat copay immediately. This is a massive advantage over standard HDHPs where you pay full price until the deductible is met.

The Hidden Trap: Integrated vs. Separate Deductibles

One of the biggest mistakes people make when switching plans is ignoring how deductibles interact with prescriptions. An integrated deductible means your medical and prescription spending count toward the same total. If your plan has a $2,000 integrated deductible, you must spend $2,000 on healthcare before the insurance kicks in for most drugs.

However, many marketplace plans, particularly Silver SPDs, offer a separate benefit for generics. They waive the annual deductible entirely for Tier 1 drugs. This means you pay a small, fixed copay (like $10) from day one, regardless of whether you’ve met your medical deductible. In contrast, a plan with an integrated deductible might seem cheaper in monthly premiums but could cost you thousands more annually if you need regular medication. Always check if the plan waives the deductible for generics. This single feature can save you between $1,200 and $5,000 a year depending on your medication needs.

Step-by-Step: How to Verify Your Coverage

Don’t rely on marketing materials or general summaries. Insurers are required to provide detailed forms, but they aren’t always easy to read. Here is a practical checklist to ensure your new plan covers your specific needs:

- Get the Full Formulary: Don’t just look at the tier summary. Download the complete PDF or use the online search tool provided by the insurer. Search for your exact drug name.

- Check the Manufacturer and Formulation: This is crucial. If you take Metformin Extended Release, make sure that specific formulation is listed. Sometimes immediate-release versions are Tier 1, while extended-release is Tier 2. Also, note the manufacturer. If your current pharmacy stocks Brand X generic, check if Brand Y (preferred by the new plan) is therapeutically equivalent. Ask your pharmacist if switching manufacturers is safe.

- Verify Pharmacy Networks: A generic drug might have a $5 copay at a preferred pharmacy network but a $50 copay at a non-preferred one. Check if your local pharmacy is in-network. Mail-order pharmacies often offer 90-day supplies at lower costs, but not all generics qualify.

- Calculate Total Annual Cost: Use the plan’s cost estimator tool. Input your medications, dosage, and frequency. Compare the total out-of-pocket cost (premiums + copays + deductibles) across different plans. A plan with a higher premium might be cheaper overall if it offers better generic coverage.

Common Pitfalls When Switching Plans

Even careful shoppers can slip up. Based on user feedback and industry data, here are the most common errors:

- Assuming All Generics Are Equal: As mentioned, some plans designate certain generics as "non-preferred" due to pricing agreements with specific manufacturers. This can move your drug from Tier 1 ($5 copay) to Tier 2 ($30 copay).

- Ignoring Strength Variations: A 500mg pill might be covered differently than a 1000mg pill. Always check the exact strength prescribed by your doctor.

- Overlooking Specialty Generics: If you take complex generics (like injectables or biologics), they may fall into Tier 4 or 5, subject to high coinsurance (e.g., 20% of the drug cost) rather than a flat copay. These costs can escalate quickly.

- Failing to Check Prior Authorization Rules: Some plans require your doctor to get approval before covering certain generics, even if they are technically on the formulary. Delays in authorization can lead to gaps in treatment.

Tools and Resources to Help You Decide

You don’t have to do this alone. Several tools can simplify the comparison process:

- Healthcare.gov Plan Selector: For marketplace plans, this tool allows you to input your medications and see estimated costs side-by-side.

- Medicare Plan Finder: If you are on Medicare, this official CMS tool lets you compare Part D and Medicare Advantage plans based on your specific drug list.

- Insurer-Specific Calculators: Many large insurers (like UnitedHealthcare, CVS Caremark, or Elevance Health) offer online calculators that provide more granular estimates than government sites.

- Your Pharmacist: Pharmacists are experts in formularies. Bring your potential new plan documents to your local pharmacist. They can tell you instantly if your current medications are preferred and suggest alternatives if needed.

Looking Ahead: Changes in 2026 and Beyond

The landscape of drug coverage is evolving. Recent regulations, such as the Inflation Reduction Act, have introduced caps on insulin costs and out-of-pocket maximums for Medicare beneficiaries. By 2026, we are seeing more standardized options in the marketplace, with expanded Silver SPD plans offering predictable $10-$20 copays for generics regardless of deductible status. Additionally, AI-powered tools are emerging to help users compare formularies more accurately, reducing enrollment errors.

However, complexity remains. With some plans introducing more granular tiers (splitting generics into preferred and non-preferred), the need for diligent verification has never been higher. Stay informed about state-specific mandates too. For example, some states require zero copays for insulin or other essential drugs, which can significantly impact your choice of plan if you live in those areas.

What is the difference between a preferred and non-preferred generic?

A preferred generic is usually placed in Tier 1 of the formulary and has the lowest copay (e.g., $5-$10). A non-preferred generic is often in Tier 2 and has a higher copay (e.g., $20-$40). The difference usually depends on which manufacturer produces the drug and whether the insurance company has a contract with that manufacturer. Both contain the same active ingredient, but the cost to you differs.

Do I have to meet my deductible before getting generic drugs?

It depends on the plan. Many High-Deductible Health Plans (HDHPs) require you to meet the deductible first. However, Silver Standardized Plan Designs (SPDs) in the marketplace often waive the deductible for Tier 1 generics, allowing you to pay a fixed copay immediately. Always check the "prescription drug coverage" section of the Summary of Benefits.

Can my pharmacist help me choose a health plan?

Yes. Pharmacists are knowledgeable about formularies and drug equivalencies. They can tell you if a specific generic is likely to be preferred or non-preferred under various plans and advise if switching manufacturers is safe. While they cannot give financial advice, their clinical expertise is invaluable for verifying coverage details.

Why does my generic drug cost more at one pharmacy than another?

Pharmacy networks matter. Insurance plans negotiate rates with specific pharmacy chains (preferred networks). If you go to a non-preferred pharmacy, your copay may increase significantly, sometimes by 300-400%. Always check if your local pharmacy is in-network before filling prescriptions.

What should I do if my generic drug is not covered by the new plan?

First, confirm it’s truly not covered by checking the full formulary. If it’s excluded, talk to your doctor about therapeutic alternatives that are on the formulary. If no alternative exists, you may need to request a formulary exception or prior authorization from the insurance company, though approval is not guaranteed.

Medications

Medications